The integrated e-commerce based on Tmall and JD.com has a market share of nearly 90% in the maternal and infant B2C market, and the vertical e-commerce share is around 10%. Tmall, Jingdong and other integrated e-commerce platforms rely on flow advantage, category synergy, and scale purchasing ability to enter the maternal and child market, which is superior to the maternal and infant vertical e-commerce share.

The maternal and child retail industry has expanded steadily, and online channel growth has been fast and the proportion has continued to rise. According to Roland Berger's data, the overall channel revenue in 2015 was 1.02 trillion yuan, and it is expected to reach 1.83 trillion yuan by 2020, CAGR = 12.3%.

The retail industry has expanded steadily, and online channels have grown at a faster rate and the proportion has continued to rise. According to Roland Berger's data, the overall channel revenue in 2015 was 1.02 trillion yuan, and it is expected to reach 1.83 trillion yuan by 2020, CAGR = 12.3%.

Among them, 69.41 billion yuan (68%), CAGR=9.6% in 2015-2020, 326.6 billion yuan (32%) in online, and CAGR=17.5% in 2015-2020. As the online growth rate is faster than the offline, it is expected that the future ratio will be further increased to 40%.

Offline channels: fierce competition, the relative advantage of maternal and child stores is obvious

Offline channels: shopping center / department store scale leading, maternal and child stores faster growth

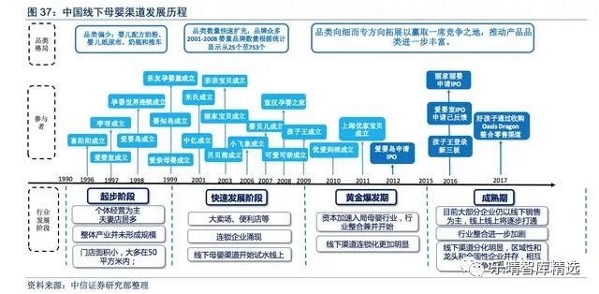

Industry Status: China's maternal and child channels have experienced four stages, and the industry has entered a mature stage. The capital competition has escalated, and the era of staking is gradually coming to an end. As the barriers to entry increase and internal integration adjustments come, enterprises with competitive advantages are expected to stand out and channel concentration is expected to increase in the long run.

From the channel structure point of view: due to the obvious social characteristics of the maternal and child industry, although the online channel growth rate is relatively fast, offline is still an irreplaceable important existence.

There are several channels under the line: maternal and child stores (31% in 2016), supermarkets (19%), and department stores (40%). Looking ahead:

1. Maternal and baby stores: According to Roland Berger's forecast, CAGR is 18.2% in 2015-2020, and the growth rate is the highest in several channels online.

The main reason is that in the context of maternal and child product consumption upgrade, branding and high-end, the relative advantages of chain maternal and child stores with complete categories, professionalism and iterative related service models are more prominent.

Specifically, the participants have a full range of channels including food, cotton-spun products and utensils, as well as services such as swimming and touching for infants and toddlers; and mothers and babies who are solely responsible for food, clothing and utensils. Channel provider.

(1) The product category is rich, the brand is numerous, and the selection range is wide;

(2) Have professional shopping guides to meet consumers' demand for one-stop shopping and professional services;

(3) Chain operation is beneficial to control operating costs, and quickly establish brand effect to achieve scale growth. The coverage of consumer groups is broad and flexible, and some are targeted at the mass consumer groups, and some are targeted at the middle and high-end groups.

2. Supermarket convenience store: It is estimated that CAGR will be 9.9% in 2015-2020, and the growth rate is relatively stable.

Specifically, infants and young children's milk powder, complementary foods, disposable diapers, toiletries and other fast-moving products are the main products, and the category is less & the brand advantage is not prominent.

The display area of ​​the goods is small, the brand advantage is not prominent, relying on the large passenger flow of the store and the supermarket, and the entry cost leads to higher operating costs, which is suitable for the sales of the mass-market low-end products with large single-unit sales, and thus the category is limited. There are also fewer specifications for appliances. Mainly for the mass consumer.

3. Department store hypermarket: It is estimated that CAGR will be 10.0% in 2015-2020, and the growth rate is also relatively stable.

Specifically, the products are mainly concentrated in infant cotton textile products, toys, durable consumer goods such as lathes and functional clothing for pregnant women with higher gross profit margins. The shopping environment is better, usually the brand has a higher visibility, has an advertising effect, and relies on the high passenger flow of the mall to ensure sales performance.

However, the operating expenses are relatively high. Usually, there are deduction points in the shopping malls, which are only suitable for selling goods with higher gross profit margins. For the middle and high-end consumer groups.

In terms of category structure, products such as milk powder and disposable diapers accounted for the largest proportion of sales revenue, but the gross profit margin was lower. Non-standard items such as toys and clothes are the main profit categories of channel dealers.

Maternal and child shop model: rapid expansion, but the pattern is scattered, the concentration is low

According to Euromonitor statistics, the market size of China's maternal and child stores reached 105.6 billion yuan in 2015, and CAGR was 19.63% in 2010-2015.

According to Nielsen, the number of maternity stores increased from 52,321 in 2012 to 98,168 in 2016, with CAGR=17%. At the same time, the maternal and child shop has the following two characteristics:

Compared to supermarket convenience stores and department stores, maternity stores can provide additional services, so the price of the product actually includes the added value of the service.

Relative to the online, the price is relatively separated, there is no online transparency, and the convenience of buying and using, the offline is relatively safe, assured, can be returned, and there are additional services, consumers are willing to pay a premium for this.

Competitive landscape:

(1) The degree of concentration is low and the pattern is extremely scattered. According to income, the sum of the incomes of the largest child king, baby-infant island, Liying room and baby-friendly room is less than 10%.

(2) Each of them “occupies the mountain as the king†and presents regional characteristics. Domestic large-scale maternal and child commodity chain retail enterprises are relying on major cities to gradually expand geographical coverage by establishing branch offices and chain operations in multiple regions, and are committed to becoming a professional maternal and child commodity retailer.

However, the cost of operation across large areas is relatively high, and it is more difficult for foreign companies to enter the local market than local leading enterprises. Therefore, the operation of maternal and child commodity chain retail enterprises has obvious regional characteristics.

Online channels: the advantages of integrated e-commerce are obvious, vertical e-commerce & social e-commerce still to be broken

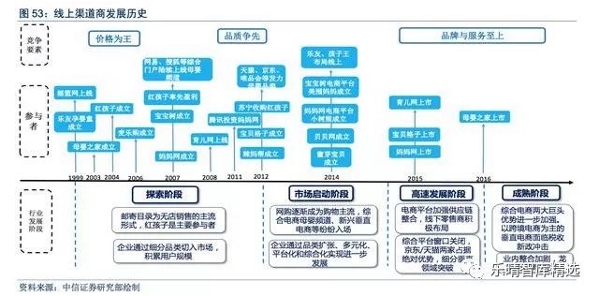

Development history: the comprehensive platform competition pattern is gradually clear, and vertical e-commerce is in the stage of differentiation

The maternal and child industry has undergone four stages of development and precipitation, and has entered the stage of maturity. From the perspective of the pattern, the two advantages of online integrated e-commerce are further strengthened, and the vertical e-commerce based on cross-border e-commerce is partly affected by the impact of the new taxation policy and the consolidation of integrated e-commerce, and the industry consolidation is intensified.

According to iResearch data, in 2015, China's mother-infant online channel transaction scale was 360.6 billion yuan, and CAGR 76% in 2012-2015. It is expected to reach 767 billion yuan in 2018 and CAGR 29% in 2016-2018.

Among them, the proportion of B2C from 47% in 2014 to 65% in 2016, the increase is due to the obvious advantages of B2C in terms of service quality, product security and after-sales service.

The integrated e-commerce based on Tmall and JD.com has a market share of nearly 90% in the maternal and infant B2C market, and the vertical e-commerce share is around 10%. Tmall, Jingdong and other integrated e-commerce platforms rely on flow advantage, category synergy, and scale purchasing ability to enter the maternal and child market, which is superior to the maternal and infant vertical e-commerce share.

According to the data of Analysys think tank, the market share of Tmall, Jingdong, Vipshop and Suning in China's maternal and infant B2C market in 2017Q3 is 50, 26%, 4 and 2% respectively.

Mode Discussion: Integrated e-commerce aggregates massive flows and is profitable through comprehensive categories

Because the mother-infant population has the characteristics that the population is easy to lock and the demand is easy to judge, each e-commerce platform will focus on the maternal and child categories, as a flow portal, attracting a large number of users and then making profits through other categories.

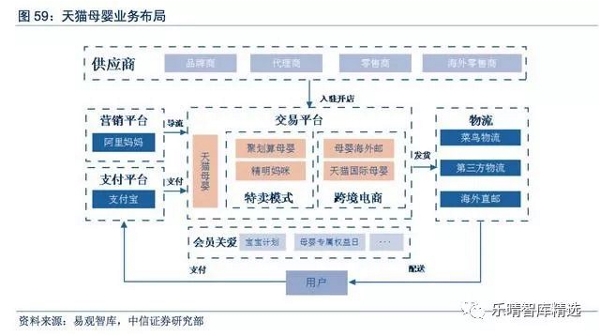

1. Tmall: The platform has obvious advantages, and the commission and advertising model are stable.

With the advantage of the platform to aggregate a large amount of traffic, through the rake and advertising to make a profit, the main features are two:

(1) Naturally equipped with non-standard products such as clothing and toys, the structure of maternal and baby products is more balanced (compared with Jingdong's milk powder and paper diapers), and the profitability is stronger.

According to the star map data, the market share of Jingdong and Tmall in B2C of 2016 milk powder was 44.4% and 37.7%, respectively. According to KarterRetail data, Jingdong and Tmall accounted for 37% and 36% respectively in B2C.

(2) The long-term business relationship with third-party milk powder and paper diaper sellers is stable and the profit is stable.

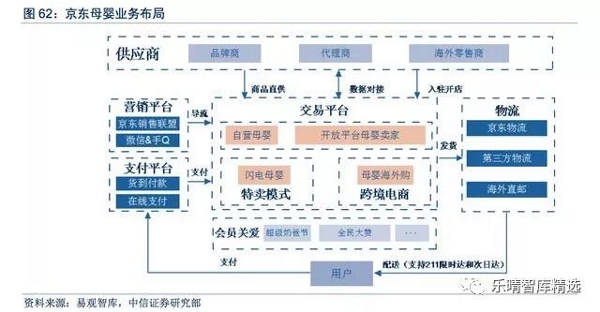

2. Jingdong: self-supporting mother and baby platform + open-type maternal and child platform sellers

There are both self-supporting mother and baby platforms, as well as open maternal and child platform sellers, as well as special sales modules and cross-border e-commerce modules. In the self-operated field, Jingdong and 12 famous brands of milk powder and diapers such as Kao and Wyeth signed a large purchase order of not less than 20 billion yuan, and cooperated in the fields of product customization, big data analysis and marketing openness;

With the advantages of logistics and warehousing accumulated by itself, we can quickly make large-scale, but at present, paper diapers and milk powder account for a high proportion, price is transparent, and profitability is poor.

In the future, the company will optimize the cost structure through the fine-grained operation of the products, and rely on the advantages of the platform to make high-margin products and rich in categories.

Future strategies and ideas:

Jingdong Supermarket cooperated with Beiquan Power Channel to sink, and opened 5,000 “Jingdong Maternal and Child Experience Stores†in the country within three years, focusing on third- and fourth-tier cities, bringing consumers a high-quality, efficient and convenient shopping experience;

Jingdong Supermarket and Mama Network launched the “King Mom Programâ€, and the two parties will work together to provide brand-wide full-process marketing solutions from consumer scenarios to consumption decisions.

Mode Discussion: Vertical E-commerce faces certain pressure in the short term

In the integrated e-commerce mother-infant category, in order to achieve the purpose of flow "resonance", the mother-infant vertical e-commerce is also constantly entering the market, but compared with the integrated e-commerce, the vertical maternal and child e-commerce living space is extremely limited.

(1) The integrated e-commerce attracts the flow by virtue of the platform advantage, and makes profits through the better maternal and child product structure and other category products, which has occupied the vertical e-commerce living space to a certain extent;

(2) After the introduction of the new taxation policy, the cost advantage of some cross-border e-commerce is further weakened. At the same time, the Internet price ratio is direct and transparent, resulting in fierce price competition for online maternal and child products and relatively sensitive consumers. Cross-border e-commerce mainly deals with limited profit margins for milk powder and paper diapers, while high-margin, high-margin toys & apparel categories The scale of online sales is small, and the current situation of income and no profit is difficult to change significantly in the short term.

(3) The maternal and child vertical e-commerce platform is limited by products. The user structure is single, mainly concentrated in the mother group, and it is difficult to superimpose the service and ensure the quality. Therefore, it is more difficult to cultivate customer stickiness than the integrated e-commerce and offline channels. resistance.

In the long run, leading cross-border e-commerce companies will expand their products, reduce costs and reduce intermediate links, and strive for brand endorsements. Honey buds and babe nets will start from the main diaper and gradually cultivate internal strength, and through the mining of high gross profit. The category enhances profitability, and in the future it is more likely to form a small and beautiful advantage vertical brand e-commerce.

Mode Discussion: It is more difficult for social e-commerce to realize short-term traffic

Social platforms: Social attributes are difficult to form effective purchases. The reality is that most mothers enter the community not to buy things, but to simply communicate and obtain information. The user's purpose is very strong, the platform attributes and user matching are not high, and the conversion rate is very low.

In the long run, the maternal and child groups with strong social attributes and the increasingly active maternal and child community ensure the continuous flow of social e-commerce. It is believed that in addition to advertising, social e-commerce will continue to improve customers in the future by returning content, cultivating marketing and services. Dependence, and find a more reasonable and effective way to achieve liquidation.

Summary: There are advantages and opportunities for growth both online and offline.

Factors such as the strong social attributes of maternal and child types and the transparency/convenience of online prices determine the importance of online/offline. In 2015, the overall channel revenue scale was 1.02 trillion yuan, and the offline/online revenues accounted for 68%/32% respectively. It is expected that the online channel share in 2020 is expected to further increase to 40%.

Under the offline channel, maternal and child stores/department stores/supermarket convenience stores are expected to coexist for a long time.

1. Maternal and baby stores hope to maintain rapid growth with a wide range of products/multiple brands/professional services, CAGR = 18.2% in 2015-2020.

Among them, the big store model category/layout shopping center/extension service is expected to expand efficiently; the small store model selects SKU to create explosions/low rental costs, small and beautiful regional operations, expecting integrators to appear.

2. Department stores hypermarkets/supermarket convenience stores have their own advantages, and are expected to maintain a compound growth of around 10%.

On the online channel side, the integrated e-commerce platform looks at the flow advantage of the maternal and child industry, and pours resources to create a maternal and child entrance. The vertical platform is undergoing a mode upgrade, and it is expected to develop in a small and beautiful direction.

Long-term outlook: cross-border operation + user and traffic management is the core

Commodities, channels, and service providers have blurred boundaries, and comprehensive and cross-border operations have emerged.

Referring to the world's major infant industry participants, we found that when the baby market develops to a certain stage, the margins of goods, channels and services are becoming more and more blurred. On the one hand, many baby-child enterprises are deeply rooted in their fields, and the upstream and downstream are extended to control supply. The chain has a comprehensive advantage. On the other hand, many companies also participate in the baby market through group-based models across categories and even across borders.

User assets will become core business assets

The baby industry has gradually entered a mature period, supporting the scale of the previous growth, competition and channel dividends have been weakened. The business model has reached a watershed. The development of the industry has shifted from “scale expansion†to “structural optimization and service superpositionâ€. It is difficult to maintain stable customer relationships only in commodities. The competition of maternal and child platforms in the future is essentially the competition of user resources and traffic. Who can control

Core and stable user resources can control the sustainability of high profitability and profitability. The “Service + Commodity†model enhances gross margins, enhances the core profitability of the company, and delivers profitability stability and sustainability.

Kangti has patented technology and domestic leading high-end professional production line to create exquisite and high-quality titanium water ware: pure titanium outdoor water cup, pure titanium office water cup, pure titanium coffee cup, double-layer titanium water cup, etc. Compared with ordinary water cup, Titanium Cup is lightweight, portable, antibacterial and fresh-keeping, not rust and corrosion resistant, which is very suitable for outdoor travel For office use, the titanium cup can be heated by direct combustion, making it a good companion for outdoor camping

Titanium Coffee Mug,Toaks Titanium Cup,Double Wall Titanium Mug,Titanium Mugs

Suzhou Xinjingyi Titanium Products Co. , Ltd. , https://www.puretitaniumcookware.com